In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired. On the flip side, if prices fall during the year, FIFO will have the lowest ending inventory and the highest cost of goods sold. Michelle Payne has 15 years of experience as a Certified Public Accountant with a strong background in audit, tax, and consulting services. She has more than five years of experience working with non-profit organizations in a finance capacity. Keep up with Michelle’s CPA career — and ultramarathoning endeavors — on LinkedIn. It is the amount by which a company’s taxable income has been deferred by using the LIFO method.

Methods of calculating inventory cost

- To better understand the FIFO inventory method, imagine a gumball machine.

- Let’s say that a new line comes out and XYZ Clothing buys 100 shirts from this new line to put into inventory in its new store.

- The gumballs at the bottom of the machine were likely the first ones added.

- We’ll explore how the FIFO method works, as well as the advantages and disadvantages of using FIFO calculations for accounting.

- Many industries with perishable goods use FIFO, including food and beverage, pharmaceuticals, and retail.

Keeping track of all incoming and outgoing inventory costs is key to accurate inventory valuation. Try FreshBooks for free to boost your efficiency and improve your inventory management today. The bad news is the periodic method does do things just a little differently. FIFO offers a clear path to inventory management and financial integrity.

Improve Inventory Management with FreshBooks

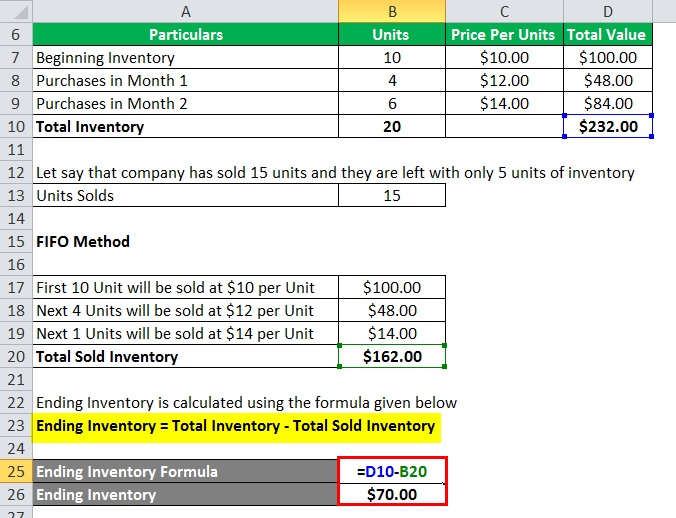

Accounting software offers plenty of features for organizing your inventory and costs so you can stay on top of your inventory value. FIFO is calculated by adding the cost of the earliest inventory items sold. The price of the first 10 items bought as inventory is added together if 10 units of inventory were sold. when can i file taxes 2021 The cost of these 10 items may differ depending on the valuation method chosen. There are balance sheet implications between these two valuation methods. More expensive inventory items are usually sold under LIFO so the more expensive inventory items are kept as inventory on the balance sheet under FIFO.

Average Cost Method of Inventory Valuation

Jeff is a writer, founder, and small business expert that focuses on educating founders on the ins and outs of running their business. Specific inventory tracing is only used when all components attributable to a finished product are known. Upgrade your business operations with modern software solutions tailored to your needs. Inventory is valued at cost unless it is likely to be sold for a lower amount.

Throughout the grand opening month of September, the store sells 80 of these shirts. All 80 of these shirts would have been from the first 100 lot that was purchased under the FIFO method. To calculate your ending inventory you would factor in 20 shirts at the $5 cost and 50 shirts at the $6 price.

With FIFO, older inventory is theoretically purchased at a lower price than newer inventory. This is because the newer inventory is purchased at a higher inflationary value. Thus, the lower cost of the older inventory at the current (higher) inflationary value leads to higher net income. Conversely, this method also results in older historical purchase prices allocated to the cost of goods sold (COGS) and matched against current period revenues.

FIFO is popular among companies because it simplifies tracking the flow of costs—the goods purchased first are the ones sold first. Grocery store stock is a common example of using FIFO practices in real life. A grocery store will usually try to sell their oldest products first so that they’re sold before the expiration date. This helps keep inventory fresh and reduces inventory write-offs which increases business profitability.

In managing a wide variety of inventory needed for projects, FIFO helps prevent a buildup of materials that might deteriorate over time. Optovue, a global manufacturer of ophthalmic imaging equipment, uses mobile software to keep FIFO rules in check while also simplifying traceability compliance. With the assistance of technology, the company operates with near-perfect inventory accuracy. The FIFO method inventory valuation is commonly used under both International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP).

FIFO can be useful during periods of inflation when higher profits may positively affect investor perception. On the other hand, LIFO shows reduced profitability, which can provide tax advantages, in particular short-term tax relief. FIFO may help contribute to higher ending inventory balances on the balance sheet, but LIFO does the opposite. Instead of increasing inventory balances, the ending value is lower, leading to lower net income.

In particular, a more conservative approach to inventory valuation more closely aligns with standard accounting practices. The FIFO method of inventory valuation results in an overstatement of gross margin in an inflationary environment and therefore does not necessarily reflect a proper matching of revenues and costs. For example, in an environment where inflation is on an upward trend, current revenue will be matched against older and lower-cost inventory items, resulting in the highest possible gross margin. FIFO is a straightforward valuation method that’s easy for businesses and investors to understand. It’s also highly intuitive—companies generally want to move old inventory first, so FIFO ensures that inventory valuation reflects the real flow of inventory. In some cases, a business may not actually sell or dispose of its oldest goods first.

Leveraging demand forecasting capabilities, you can gain insight into your changing inventory needs while also minimizing excess stock issues and obsolescence problems. Adopting a proactive FIFO approach supported by technologies and automation tools can help you enhance overall supply chain efficiency, resulting in improved customer satisfaction and cost savings. Additionally, properly labeling and storing all of your inventory with identification markers such as batch numbers, expiration dates, or production dates is especially helpful for FIFO. Organizing your inventory systematically enables you to quickly locate items that have been in stock for a longer time and prioritize them for sale or use. You can simplify these processes with inventory and order fulfillment software to automate tasks like inventory tracking, label creation, and product categorization. While FIFO refers to first in, first out, LIFO stands for last in, first out.